I recently read a paper titled “Quality and Inequality, Taste, Value, and Power in the Third Wave Coffee Market,” in which the author, Edward F. (Ted) Fischer talks about tastemakers; some of the most-popular cafe’s, which are able to leverage their influence to steer consumer preference in the coffee market.

The tastes of the Barista consumers – and, even more importantly, of the roaster and baristas and their tastemaker peers at Stumptown, Intelligentsia, La Colombe, Counter Culture, and the other “Third Wave” coffee pioneers – have serious consequences for folks in Colombia, Yemen, Vietnam, and the other tropical countries that produce coffee.

(Fischer, 2017)

One critique made by the author is that because these tastemakers influence the market’s preferences, they have a power advantage over producers and the producers are left reacting to market desires rather than influencing the market themselves. Fischer states that what tastemakers value and what producers value are different and I would certainly agree. That difference in what is valued is not limited to coffee, but is common in many other crops, both horticultural and agricultural. More on this later.

It’s not just that the two ends of the supply chain have different values. I argue that the two ends of the value chain have different but related and dependent products and different but complimentary skills. Furthermore, I would argue that the tastemakers are essential to the success and progress of the producers and vice versa. Therefore, to truly empower the farmer, I recommend the farmer leverage their unique skills as a farmer, while depending on the unique skills of the tastemakers in order to coexist and improve the effectiveness, and therefore the livelihood of the entire chain.

Conversely, the tastemakers are dependent on the farmers to provide the right products to steer the culture. It goes without saying that a tastemaker must have access to the particular taste profile being championed. Consider a particularly innovative farmer who experiments with different products. He or she could introduce the tastemakers to a new taste profile and allow the tastemaker to begin the process of establishing legitimacy of that particular taste.(Maguire, 2019)

In this way, farmers sit at the very beginning of the tastemakers’ pathway towards validation. That pathway can be summarized like this (again, drawing from Macquire):

Different products, different goals

The two ends of the coffee value chain have completely different goals and produce completely different products. At the production end, the farmer is producing a raw material; coffee cherries. There are often cases in which producers do mill their own cherries to produce unroasted, green coffee. There are also farmers who roast and sell their own coffee and in those cases, the farmers maintain a considerable amount of control over the product. But not all farmers, arguably not many, want that. They want to be farmers.

In the case of farmers who just want to be farmers, they are producing a crop that when harvested, has a value to intermediary players chain who can then sell the product to roasteries and cafes who turn the intermediate product into a consumable product. The intermediaries have language skills, sales skills, marketing skills, marketing channels, etc., that make them successful at finding an intermediate product that a roaster and/or cafe wants to buy and turn into a consumable product.

Almost 80% of the world’s coffee is produced by smallholder farmers. (“Coffee Farmers - Fairtrade Foundation,” 2016) These smallholder Farmers most likely were born and raised in remote, mountainous regions of developing countries, likely with minimal education, minimal exposure outside of their remote region, and largely without the disposable income (Sowell, 2015) that would allow them to experience the kind of consumption of coffee that happens in developed nations, especially in the Third Wave coffee scene.

Without the language skills, exposure to and an understanding of conspicuous consumption, marketing techniques, etc, farmers have a hard time marketing and selling their intermediate product to roasteries and cafes. The same problem exists on the opposite end of the chain; ‘direct trade’ is challenging primarily due to language and distance barriers, but also because of cultural barriers.

It's all about the skills

Another reason why those closer to the consumer are the tastemakers is the difference in skills. The tastemakers don’t generally have the skills to produce the intermediate product — most times they don’t even have the proper geographical needs i.e., a mountainous, tropical climate. But they do have the roasting skills, the cupping skills, the marketing skills, the sales skills, etc. to create a symbolic value in the product that makes it more desireable to the end consumer.

The Third Wave of coffee is focused on the story; the story of the producer, where he or she is located, how he or she grows and produces the coffee, etc. This story then drives ethical consumption, which (hopefully) further benefits producers with its goal of responsibility towards society.

Yes, this creates a ‘shared, aesthetic valuation’ and yes, all of the players throughout the value chain have economic interest at stake. But when leveraged in the right way, these things benefit the entire value chain.

Tastemakers drive consumption

The entire value chain depends on consumption and conspicuous consumption especially drives up coffee prices. Consider the history of the three waves of coffee. The First Wave of coffee was wide-spread consumption of Foldgers Crystals (instant or soluable coffee), Maxwell House (good to the last drop!) and in general, low-quality coffee. The coffee was low-quality for several reasons.

We didn’t have a solid understanding of coffee staling. We now know that ground coffee, when exposed to oxygen, has a fresh life measured in minutes. Whole-bean coffee has a fresh life of just a few weeks once exposed to oxygen. Before we fully understood the staling process in coffee, we routinely drank old, stale, flat coffee—we just weren’t aware of it. We didn’t know there was a better way. We needed the tastemakers to tell us. We needed innovation in anti-staling measures, such as Illy’s use of nitrogen-flushing, and we needed tastemakers to validate the higher-quality coffee produced when staling is avoided.

Another reason the coffee was low-quality is because most coffee was a melange of different qualities of coffee breeds, processing techniques, etc. Even today, instant or soluable coffee is very often a mixture of poor quality coffee. It often has robusta mixed in, as well as defective beans that hve been damaged by insects, are rotten, moldy, etc. There are two economically important breeds of coffee tree; arabica and robusta. Arabica has better sensory qualities (flavor, aroma, etc) and robusta has better agricultural qualities (pest/disease resistence, greater yield, etc). Thanks to the tastemakers of the Second Wave, we’re drinking less instant coffee and more espresso-based coffee and especially of better quality than what was the norm in the First Wave.

Enter Starbucks. Regardless of what you may think of Starbucks, they are largely responsible for introducing the mainstream West, especially the U.S. to espresso-based drinks. They were largely responsible for ushering in the Second Wave of coffee consumption, which laid the groundwork for Specialty, or the Third Wave of coffee. Starbucks largely drove the early diffusion and then general validation of higher-quality coffee.

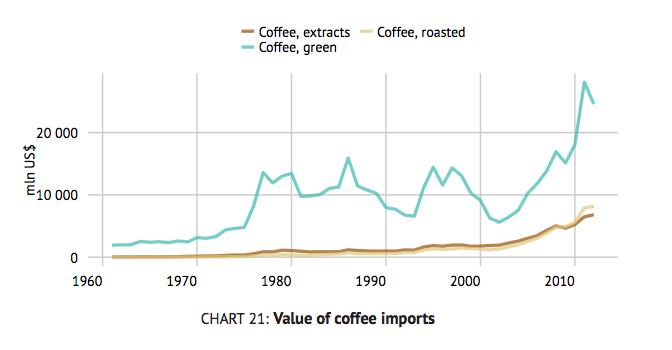

The result of the popularity and the ubiquity of Starbucks increased consumption drastically. An eventual outcome of that increase in consumption has been a significant increase in the value of coffee in all its forms, but especially green, un-roasted coffee.

See also: What Is Specialty Coffee

Part of the solution

Part of the solution to the problem of producers reacting to the preferences generated at the consuming end of the market is through innovation — by driving the tastemakers’ pathway. They can do this by baking-in optionality to their business.

See also: Producers’ Optionality

Optionality for coffee farmers means planting different cultivars and varieties around their farm, experimenting with what breeds perform best where. It also means if they mill their own coffee, to experiment with different milling techniques in an attempt to emphasize novel and unique aspects of a given coffee. This will produce innovative product options. These innovative product options can then be vetted by tastemakers. If the innovation gains validation among tastemakers, they can champion it, diffuse it, and guide it towards general validation, which would be market acceptance at a broad level.

I would also argue that Q Graders, acting as go-betweens for farmers and roasteries and cafes, have the ability to reduce the negative impact of tastemakers on farmers. Through a defined and shared lexicon, or language of quality, Q Graders can help communicate the goals with both sides, as well as how to reach those goals. For example, currently the predominant flavor profile of Third Wave coffee is a floral, fruity character. Things that contribute to that are the processing method, the breed of coffee tree, the altitude at which it was grown, etc. Part of the training in becoming a Q Grader is learning these things so that Q Graders can bridge that gap between the two ends of the value chain.

A good Q-grader can work with a smallholder farmer to understand which coffee breeds provides good yield, good pest and disease resistance, as well as a good sensory profile in the final bevarage. They can also advise on the various milling processes one can use to manipulate and accentuate those sensory profiles.

A larger cultural universe is important not simply because of the products, technologies and knowledge that are transferred—important as these are—but also, and perhaps equally or more important, because people seeing repeatedly how things have been done differently by others in different places can break through the normal human inertia that keeps people doing the same things in the same familiar ways, for generations or even centuries, as happens in many geographically isolated societies.

(Sowell, 2015)

Bridging the information gap between consuming trends and producing techniques will empower producers. They will have a better understanding of what the trends are and how to accommodate them.

See also: Local Consumption Wins in Brazil and Colombia

National Jury-a panel of tastemakers

The Cup of Excellence (CoE) is a coffee competition and auction system that strives to find the best-of-the-best a producing country has to offer and then sell that coffee at the highest amount the market will bear, through an auction process. Part of the explicit process of CoE is the formation of what they call a National Jury.

They are the gate-keepers for the competition and only the cup profiles they chose during pre-selection continue on to compete. I really like the idea of the national jurists defining the cup profile of the best of their best, rather than having an international group define it.

See also: Cup of Excellence, Indonesia

In the context of the CoE, the National Jury is a panel of empowered, local tastemakers who define what is an excellent coffee from their country. And more importantly, in this fashion the National Jury can be the very beginning of the virtuous cycle that is often referred to as local consumption, in which some of the best coffee a country produces remains and is enjoyed within the country. Local consumption enables a national pride in what that country can produce. And in that way I think tastemakers serve a very important role. Local producers and coffee professionals can point to CoE successes from their country and say ‘that represents the level of excellence my country can attain in coffee production.’ That is quite empowering.

See also: Increasing Local Consumption

The coffee market needs tastemakers in order to grow and improve. We need experts who explore coffee and inform us on what they have learned and how we can use that knowledge to become better consumers. As we become better consumers, more money flows through the value chain and eventually finds its way to the producers. The system isn’t perfect but its not intractable nor rigged — it’s complex.

- Fischer, E. F. (2017). Quality and inequality: Taste, value, and power in the third wave coffee market (MPIfG Discussion Paper 17/4; Number 17/4). Max Planck Institute for the Study of Societies. http://hdl.handle.net/10419/156227

- Maguire, J. S. (2019). Taste, Legitimacy, and the Organization of Consumption. In F. F. Wherry & I. Woodward (Eds.), The Oxford Handbook of Consumption (pp. 195–213). Oxford University Press. https://doi.org/10.1093/oxfordhb/9780190695583.013.8

- Coffee farmers - Fairtrade Foundation. (2016). In Fairtrade Foundation, Farmers and Workers. https://www.fairtrade.org.uk/farmers-and-workers/coffee/

- Sowell, T. (2015). Wealth, Poverty and Politics: An International Perspective. Basic Books.